The Changing Form of External Financial Flows

In late 2024, the Institute of International Finance (IIF), the advocacy arm of global finance, put out a pessimistic projection that capital flows to emerging market economies (EMEs) are likely to fall to $716 billion in 2025 from an estimated $944 billion in 2024. The latter figure was a significant improvement as compared with the esƟmate of $682 billion in 2023. These figures include both foreign direct investment flows ($426 billion) and portfolio flows to bond and equity markets. The volatility in the laƩer is normally much higher. Thus, the IIF estimates that portfolio flows amounted to $273.5 billion in 2024, well above the $177.4 billion in 2023, but significantly below the $375 billion average recorded between 2019-2021.

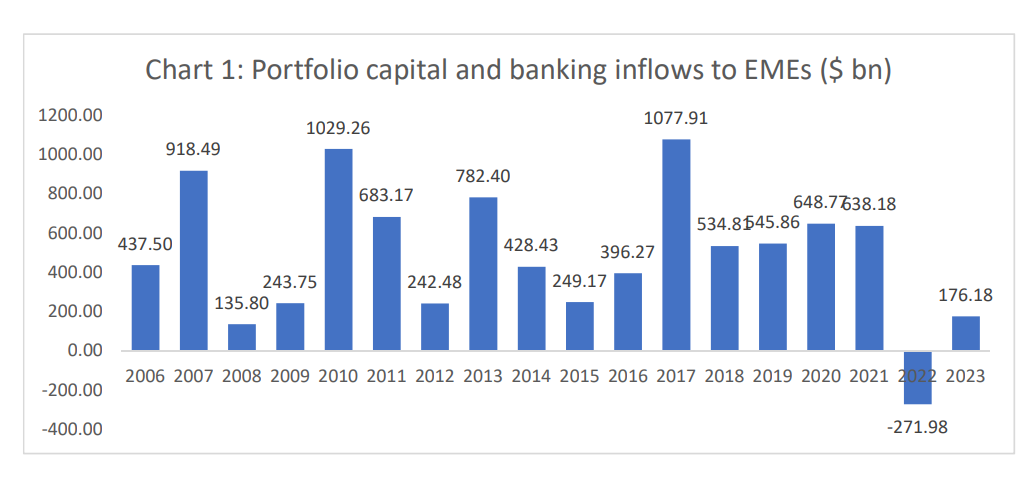

Using the IIF’s data and combining it with its own datasets and calculations, the Bank of International Settlements (BIS) has recently released a study on shifts in the composition of portfolio capital flows to emerging markets (covering 16 EMEs for bond flows and 17 for equity flows). The BIS data shows that foreign portfolio flows to EMEs, aŌer a sharp fall in post pandemic year 2022 (by $272 billion), had recovered in 2023 to just $176 billion, which was far below the flow of $638 billion recorded in 2021 (Chart 1).

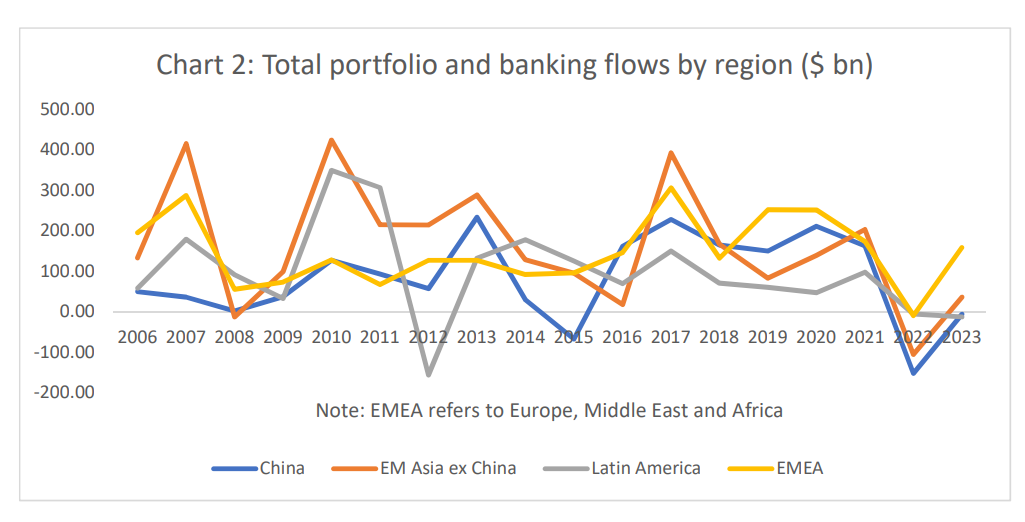

The figures point to the volatility characteristic of portfolio flows. They fell sharply from a 2007 high during financial crisis years 2008-09, then bounced back in 2010, only to fall steeply again in 2012 following the sovereign debt crisis in the European periphery. They peaked again in 2017, encouraged by low interest rates in the developed economies, and then collapsed again after the pandemic and as interest rates rose in the advanced economies. As Chart 2 shows, this volatility was characteristic of EMEs in all regions—China, emerging Asia excluding China, Latin America, and emerging markets in Europe, Middle East and Africa (EMEA).

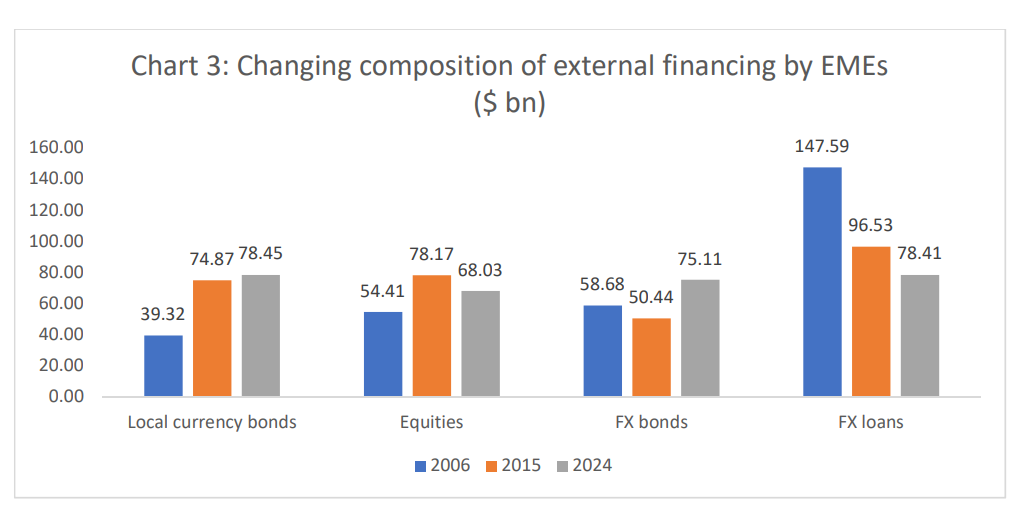

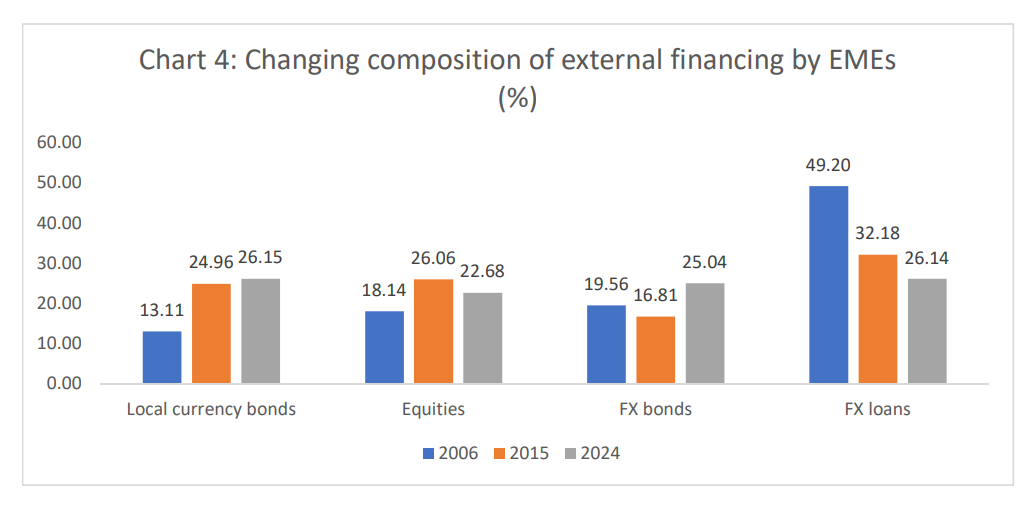

But besides this volatility, the evidence points to two other major shift in the years since the 2007 global financial crisis (Charts 3 and 4). One is a shift away from equity and forex loans to bonds in the holdings of foreign portfolio investors in emerging markets. Local and foreign currency bonds held by these non-resident investors increased in share from 33 per cent in 2006 to 51 per cent in 2024. The other is the increasing importance of external financing using local currency bonds in emerging markets. The share of local currency bonds in total portfolio capital inflows doubled from 13 per cent in 2006 to 26 per cent in 2024.

The shift to bond financing is possibly explained by the growing role of non-bank financial firms and the preferences of investment banks and hedge funds managing investments for a diverse range of investors. That shift was associated with the huge accumulation of liquidity in financial markets triggered by the easy money policies followed by central banks in the developed countries ever since the global financial crisis. A corollary of the shift has been a boom in sovereign bond issues in less developed economies, including in those identified as EMEs. In some of these EMEs, private corporations have also been issuing bonds to mop up foreign financing at interest rates that were more attractive than in domestic markets.

The riskiness of such bond issues for borrowers is higher when they are denominated in foreign currencies, since in that case the borrower bears the foreign exchange risk. If the local currency depreciates relative to the currency in which debt is denominated, then the burden of interest and amortization payments rises in terms of the local currency in which revenues predominantly accrue, for both public and private sectors. Moreover, to the extent that revenues are earned in local currency, there is the need to transform domesƟc resources into foreign currency to service external liabilities. It is the difficulty faced in such transformation that accounts for the external debt repayment difficulties that many of these countries face. This was the fallout of the ‘original sin’ that characterized the situation faced by less developed countries unable to borrow abroad in their own currency and having to borrow to cover deficits in the current account of their balance of payments.

Seen in that light, the evidence of a rise in the share of local currency bond issues in total external financing appears promising, even if such borrowing accounts for only a quarter of total external portfolio financing. What is surprising is the willingness of foreign bond investors to carry the exchange rate risk associated with such borrowing. If the currency of the country in which the borrower issues debt depreciates, it would affect the foreign currency returns associated with such lending, since less foreign currency (or currency of the lender’s country) can be purchased with the repayments made by the borrower.

There are three factors which could account for this intriguing shift in lender behaviour. First, the huge volumes of cheap liquidity available to financial investors from the developed countries in the years since the global financial crisis, when the response of central banks was a shift to a regime of quantitative easing and low interest rates. That increased the risk appetite of financial investors, who want to use the opportunity to borrow cheap and lend dear. To exploit that opportunity, they currently seem to be willing to discount the foreign exchange risk involved.

The second factor is the provision of enhanced risk premia in the interest rates associated with bond financing to cover expected foreign exchange risk. That would mean that external borrowing, even if in domesƟc currency, can be expensive and increase the domestic currency burden associate with servicing the debt. The greater the perceived exchange rate risk, the higher the interest rate.

Finally, with the flow of foreign finance associated with excess liquidity in international markets to the EMEs, the currencies of these countries have in the short term been less prone to depreciation, and in some periods and cases they have even appreciated. This provides the basis to discount foreign exchange risk, though that assessment often proves misplaced. In sum, the increase in domestic currency borrowing from foreign creditors is not all good news and can also prove to be as volatile as the flow of foreign finance to the EMEs.

(This article was originally published in The Business line on August 5, 2025).