World Economy: Out of control

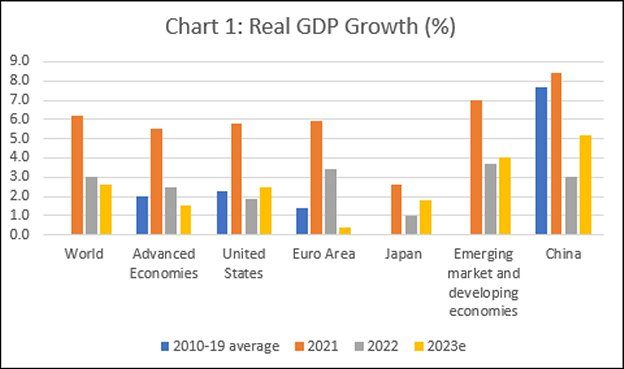

Early in 2024, the World Bank in its flagship report Global Economic Prospects, put out a message of gloom. This year could end marking “a wretched milestone: the weakest global growth performance of any half-decade since the 1990s”. Between 2021, when the world economy showed signs of recovering from the troughs of the pandemic, and 2023, growth has been decelerating almost everywhere, with the figures at 6.2, 3.0 and 2.6 per cent for the world as a whole in 2021, 2022 and 2023 respectively (Chart 1). For most advanced economies growth in 2023 was below the average recorded during the decade 2010 to 2019, with the US just staying ahead of that figure. The 2010-2019 figure matters because it captures the long-term impact of the prolonged Great Recession that followed the financial crisis of 2008 in the advanced economies. Having put the pandemic behind it, the world seems set to return to that recessionary environment.

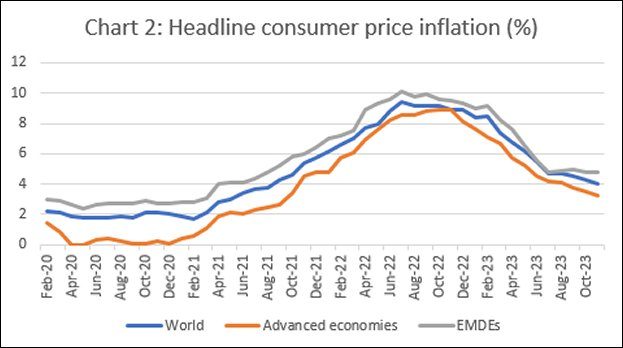

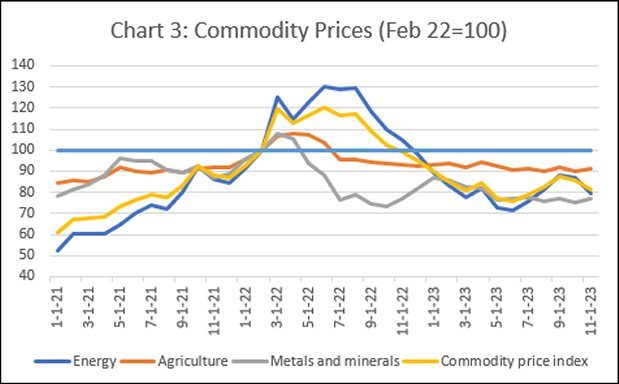

When the recovery began in 2021, the fear was of inflation not slow growth. From extreme lows during the pandemic year, consumer price indices began to climb, driven by the fact that while spending was propped up by the fiscal response to the pandemic-induced recession, supply obstructions took longer to relax (Chart 2). But even before the gradual redressal of this imbalance could rein in price inflation, the speculation in commodity markets, especially fuel and food markets, that followed the outbreak of war in Ukraine in February 2022, provided a new spur to prices. However, as it became clear that there were adequate supplies available in world markets, that speculation receded, as did inflation from the peak levels it touched in third quarter of 2022. Not surprisingly, a deceleration in commodity price increases underlay the decline in the aggregate inflation rates in the advanced economies (Chart 3).

The tendency for inflation to recede was, however, attributed to the monetary response to the inflation on the part of central banks in the advanced economies, in the form of repeated increases in interest rates. In fact, inflation rates had peaked well before policy rates had touched their peaks. In the United States, for example, the Fed funds rate had been hiked only to 3.1 per cent by October 2022, from its low of 0.08 per cent in February. It was over the next few months, when the consumer price inflation rate was in rapid decline, that the Fed rate was raised to its peak of 5.33 in August 2033.

But the correspondence of the moderation of price increases and the hikes in interest rates since August 2022 has led to the view that it was the Fed’s interest rate hikes that were responsible for the success in taming inflation. This assessment was accompanied by the presumption that a collateral consequence of the rate hikes that targeted inflation was a slow down in GDP growth. The post-pandemic slide of global growth rates back to the pre-pandemic lows was read as the sacrifice needed to rein in inflation. So, it is argued, now that inflation is under control and interest rates can once again be lowered, growth would revive the moment central bankers begin to unwind their high interest rate policies. What this ignores is the fact that long years of low and near-zero interest rates from end-2008 to early-2022 had not managed to pull the advanced economies out of the slow-growth syndrome that followed the 2008 collapse.

A more convincing explanation of growth performance over this long term can be found in the fluctuations in fiscal policy. Unlike the long-term adherence to the “unconventional monetary policies” that developed economy governments have adopted, the resort to proactive fiscal policies has been much more erratic. A proactive fiscal stance was indeed adopted in response to both the 2008 crisis and the pandemic-induced sudden stop in economic activity in 2020. But in both instances, this proactive fiscal stance was quickly reversed as the fiscal hawks held out the prospect of either inflation or a downturn triggered by excessively high public debt to GDP ratios, even though the conceptual and empirical bases for argument were far from robust.

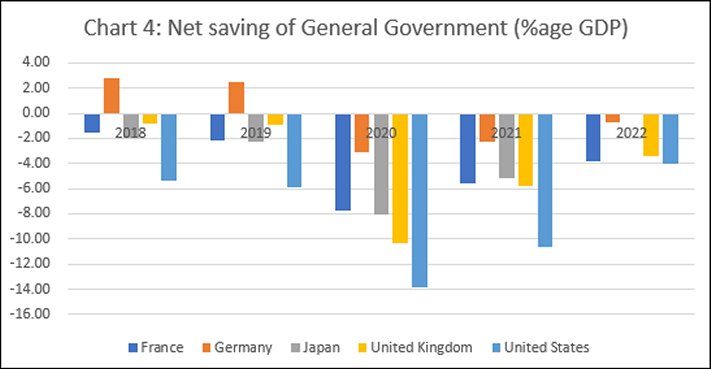

The consequence of this erratic fiscal behaviour is reflected, for example, in recent growth performance. The recovery in growth in 2021 was definitely led by the huge fiscal stimuli that governments resorted to in response to the collapse in growth in 2020. Net dissaving or deficit financed spending by the government as share of GDP spiked in 2020 in France (2.1 to 7.7 per cent), Japan (2.3 to 8 per cent), the UK (0.9 to 10.4 per cent) and the US (5.9 to 13.9 per cent). This definitely must have helped reverse the collapse in GDP, even if it contributed to the imbalance between demand and supply revival that pushed up prices (Chart 4).

But hardly had the situation begun to stabilise when governments chose to withdraw the stimulus, with deficit spending falling significantly in 2021 and 2022. Not surprisingly, growth too stalled, with the post-Covid recovery losing momentum rather quickly. Global growth that had recovered to 6.2 per cent in 2020, was down to an estimated 2.6 per cent in 2023. Given the fiscal conservatism that has gripped governments in a world dominated by finance, there is no evidence of a likely return to proactive spending to spur growth. All bets are being placed on the interest rate reductions that are likely to follow a period of subdued inflation.

There are structural factors that preclude the return to high growth in the advanced market economies. But if the current medium-term low in growth is not to continue, there is need to recognise the importance of countercyclical fiscal policies in the macroeconomic management of capitalist economies. Given the large amount of unutilised labour and spare capacity across the globe, such a policy recommends itself as a response to the current slowdown. The one economy in which policy makers abjured fiscal activism even during the pandemic is Germany. Its government did not even utilise the fiscal headroom it gave itself with emergency measures, and now finds itself unable to use that money for its climate agenda. Not surprisingly, Germany, which for long was the leader of growth in Europe, is today the worst performer.

Sustaining a proactive fiscal stance requires two other initiatives. One must be to directly curb speculative price increases driven by the conglomerates in production and trade, not least by restricting and unwinding the power of these monopolies. The other is to raise resources to finance spending by taxing the huge surpluses that are increasingly held by the rich in these countries. Public spending can indeed be financed with borrowing, but must eventually finance itself.

(This article was originally published in the Business Line on January 22, 2024)