Is it India’s Subprime?

The Indian corporate sector is grappling with a severe bad debt crisis, and as a result, the banks (public sector banks) are increasingly getting saddled with non-performing assets. Calling it India’s subprime crisis might be an exaggeration but I would just like to add ‘not yet’! Moreover in conditions such as these, with the global economic crisis in the background, it’s better to be cautious rather than looking back at the data when it’s all over. This might also help the policy makers to take regulatory steps in time to control the contagion to spread to the banking system in a big way.

Let’s look at the extent of the bad corporate debt. There are two statistics for a corporate house, which need to be looked at to understand the nature of the debt crisis. One is the amount of bank loans taken in a particular year and the other is whether the firms were financially healthy enough to take the loan in the first place.

The latter is measured by whether they made enough profits in a particular period to even cover for the interest payments accrued on past debts. As we all know any loan you take has two parts when the repayment starts: the principal (total loan amount) and the interest accrued on it (interest amount). For a firm to be financially healthy, just as a family taking a loan, it should make enough profits to cover for both [in financial terms, these are called hedged firm]. On the other hand, an unhealthy firm is one which does not even cover its interest payments [ponzi firm]. It’s anybody’s guess that the latter should not be given more loans as that is sure shot recipe for disaster. At the heart of the US subprime crisis was the fact that loans were dished out increasingly to ponzi households. That’s where the similarity lies. What was true for the household sector could be true for the corporate sector in India.

In financial jargon, the health of a firm is measured by what is called the Interest Coverage Ratio (henceforth ICR). It is a ratio of net profits to interest payments due on past debt. It being less than 1 is a danger sign for the lender because it means that the firm is not even making enough profits to pay for its past interest payment commitments let alone the principal amount.

We cover the period between 2011 and 2015 during which this process unfolded in India. We look first at a larger sample of corporate firms with consistent coverage available for these (and some other relevant variables) in the datasets available.

One might doubt whether ICR is the best measure of financial health especially for companies which take longer to generate profis resulting from time lags that assets take to build. In anticipation of this criticism, I present three other variables to present a comprehensive picture of the current corporate debt crisis but interested readers can just look at the ICR to draw their conclusions.

The three other measures are: profitability i.e. whether the firms were making positive post-tax profits; ratio of current assets to current liabilities to measure what part of the liabilities can they pay off if they were to sell their assets; debt to equity (own capital) ratio to measure how much have they stuck their own neck out compared to other people’s money in the risky adventure they are undertaking. The well accepted threshholds for these measures are 0, 0.5 and 5 i.e. firms which are making negative profits, can honour at least half their liabilities by selling off the assets, debt is five times as large as own capital respecively. Figure1 presents the share in debt of such firms in the total sample debt with these individual characteristics over the years 2011-2015.

Source: Author’s calculation, Orbis Dataset.

Note: The shares taken are out of the total debt of the sample. Since the sample remains the same across time, the trends will remain similar when the shares are taken as a proportion of total corporate debt.

It can be seen from the figure that the share of debt of firms with failing financial health has been going up since 2011. The dotted line represents how the share of bad debt has increased of those firms which could not even honour their interest commitments to the lenders and it has increased significantly since 2012. These are the ponzi firms we discussed above.

Let’s now look at something more specific with respect to some big sharks in this respect. We take 5 corporations out of the top 10 corporations (in terms of borrowing) identified by the excellent Credit Suisse 2012 report on the House of Debt and follow their trajectory for the same time period as above. Instead of looking at the stock of debt, we focus now on new borrowings during these years because it is possible to argue that if you are not in a position to pay in full the interest accrued, then on that account alone the debt can keep piling up.

What I want to show here is that most of these firms (4 out of the 5 below) were able to not only extract fresh borrowing from the banks but actually increase it even as their status continued to be ponzi! It is for this reason that I call it a potential subprime building up.

Table: Financial Health and Yearly Borrowings by Top 5 Corporate Houses

It can be seen from the table that other than Vedanta Ltd., all companies have had at least two years of being in a ponzi state (ICR<1) and yet their borrowings, with one exception, have increased every year. Let me draw an analogy here. It shows that with increasing diabetic problems in a patient (ICR falling), doctors (banks) are injecting more of sugar (loans) to the body of the patient! Very high debt-equity ratios in the table also corroborates their bad health condition.

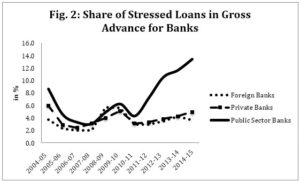

So far we have seen the story from the culprits side. Let us briefly look at the problem from the side of the banks, which has got a lot of media attention especially since the then governor, Mr. Raghuram Rajan flagged this issue initially. As can be seen from figure 2 below, most of the burden of bad loans since 2011 has been borne by public sector banks as opposed to the foreign banks or privately owned banks. The share of stressed loans, which is the sum of non performing loans and restructured loans, as a percentage of total advances made has been skyrocketting for the public sector banks.

Source: Azad, Bose, & Dasgupta (2016). “Financial Globalisation and India: Internal and External Dimensions,” MPRA Paper 63874, University Library of Munich, Germany.

In conclusion, while the banks have knowingly put themselves in the current position, the real culprits are the big borrowers and promoters who are not paying up what they had promised and the government instead of being strict on the defaulters is expecting the central bank to inject liquidity into the banking system to write off these bad loans. It will be travesty of justice if this were allowed to be done. It will just give fillip to the Malyas of the world to default with impunity since the central bank will always be made to come in as the lender of last resort.

(This article was originally published in The Hindu on February 5, 2017)