The other Face of Private Banking

A feature of banking in India that has not received the attention it deserves is the business reflected in the off balance sheet or contingent liabilities of banks. Typical of such liabilities are swaps, options and forward rate contracts involving exchange and interest rates. Globally, finalization has involved the diversification of traditional banking firms into a host of new activities such as derivative contracts and guarantees and acceptances of various kinds. These instruments are non funded in the sense that there is no actual lending, but the bank can be called upon to compensate borrowers for losses from exposures named in the contract. Since such losses and calls are most likely when the market is “tight”, the banks concerned may be forced to draw down capital at a time when accessing additional funds from the market is difficult, threatening their stability.

Exposures to these instruments have different degrees of counter party risk, that may result in losses that erode the capital of the banks. However, in most jurisdictions, unlike in the case of credit assets, there are no guidelines to provide for regulatory capital against these off balance sheet liabilities as part of capital adequacy requirements. Combined with the prospect of lucrative incomes from fees and commissions, this exemption from capital adequacy requirements encourages banks to diversify into activities that increase the volume of off balance sheet liabilities, so long as the regulatory framework permits such diversification. But associated with an increase in such contingent liabilities is an increase in exposure to risk which is not easily assessed. And early, 1986 study of off balance sheet instruments by the Bank of International Settlements had noted that “some of these are technically very complicated and are probably only fully understood by a small number of traders and market experts; many pose complex problems in relation to risk measurement and management control systems; and the implications for the overall level of risk carried by banks is not easily assessed.” Overall, diversification into off balance sheet, contingent liabilities increases the volume of risk that is not adequately assessed and is likely to be poorly managed.

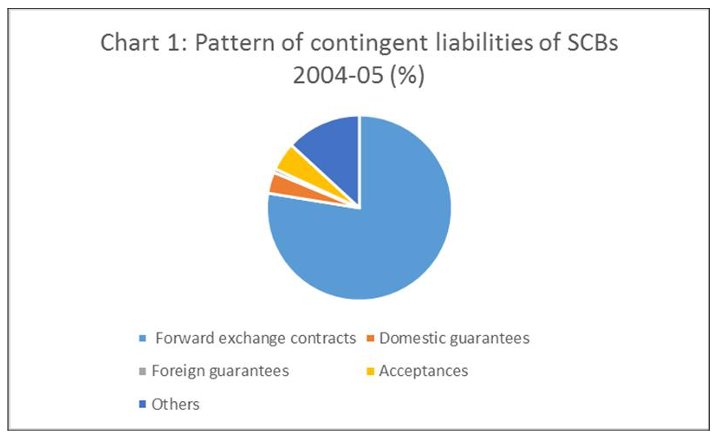

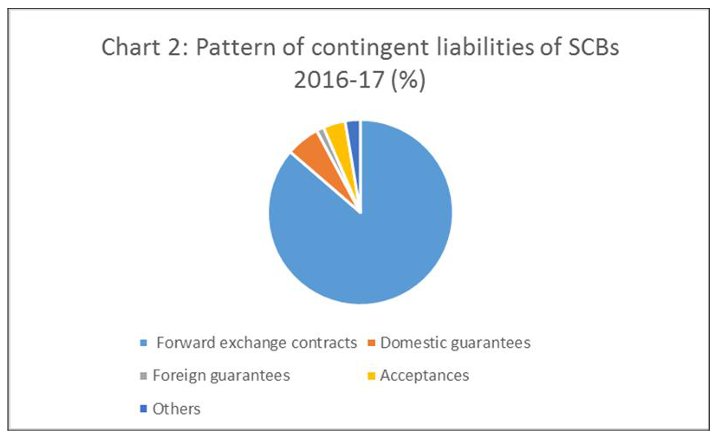

In India too, during the y volume of offers of rapid financial proliferation starting in 2005, the balance sheet exposures of commercial banks registered a more than five fold increase from Rs. 28,325 trillion in 2005 to Rs. 152,130 trillion in 2015, around which figure it has hovered since. Moreover, there has been a clear shift in the pattern of these exposures, in which forward exchange contracts (or all derivative products, including interest rate swaps) and other contingent liabilities (which includes inter alia items like (a) claims against the bank not acknowledged as debt, (b) liability for partly paid investments, (c) bills re discounted and (d) letters of credit) dominate. But while in 2004 cent of all contingent liabili05 forward exchange contracts accounted for 77.6 per ties and other instruments for 13.1 per cent, those figures stood at 86.3 and 2.6 per cent in 201617 (Charts 1 and 2). Clearly, derivatives have come to account for an overwhelming share of all off balance sheet exposures.

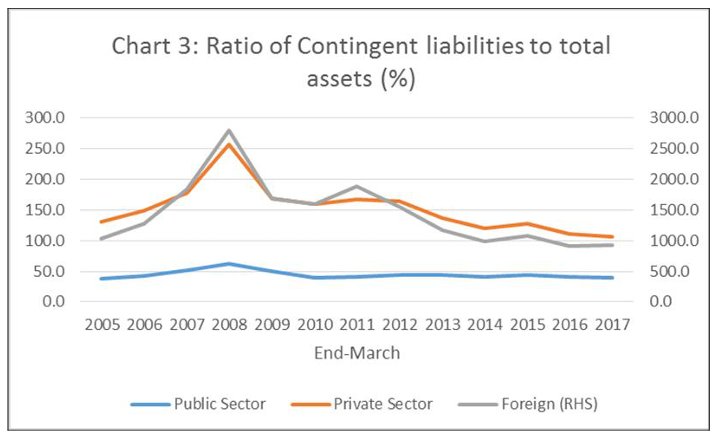

This is striking, since cautious bankers would refrain from exposing their institutions to these risks despite the fact that interest rate spreads on traditional deposit-taking and lending may be small and such activity requires setting aside costly regulatory capital to deal with credit risks and potential losses. Interestingly, this diversification in favor of contingent liabilities as an important area of business appears to be less true of public sector banks. The ratio of such liabilities to total assets of the public sector banks which rose from 38.6 per cent to 61.8 per cent between 2005 and 2008(Chart 3), or the years prior to the global financial crisis, subsequently shrank to touch39.4 per cent in 2016-17. Thus, Indian public sector banks, which also initially increased their exposure to contingent liabilities, have cut them down and have in general kept them low.

On the other hand, private sector banks and especially foreign banks, have relied hugely on contingent liabilities, exploiting the opportunities offered by the post liberalization. Though they too show similar inter temporal trends in off balance sheet exposure after 2005 as do the public sector banks, the magnitudes involved are much larger. Domestic private sector banks saw the ratio of their contingent liabilities to total assets on their books rising from 130.4 per cent in 2005 to 257.5 per cent in 2008, before registering a decline. But even in 201617 the ratio at 106.2 for private sector banks was substantially higher than the 39.4 recorded by the public sec tor banks. Finally, foreign banks saw their contingent liability to total assets ratio rise from a huge 1035.3 per cent in 2005 to 2804.4 per cent in 2008, and the decline after that took it to a still high 926.7 per cent in 201617 (Chart 3). At the end o year 2016f financial 17, while foreign banks accounted for a little more than 5 per cent of the total assets of all scheduled commercial banks, they held contingent liabilities that were equal to nearly 50 per cent of that held by the latter.

These trends have four implications. First that private banks pay less attention to the traditional intermediation role of banks, of mobilizing deposits and creating credit assets, which is less profitable. Second that these private banks are exposed to much larger risks, which are only rising, and therefore are subjecting their depositors, often attracted with higher interest rates, to excessive risk of loss. Third, very few foreign banks pursue the traditional banking business in India, preferring instead to focus on so called hedging instruments in foreign exchange and interest rates, that really involve speculative forays rather than banking activity. Fortunately, many of these banks do not mobilize much by way of deposits from ordinary depositors. Finally, the c laim that liberalization would result in private banks displacing public banks from their traditional activity has been substantially belied. The public sector remains the nation’s banker, while the private banks seem to seek out profits from speculative activity.

(This article w as originally published in the Business Line on January 1 5 , 201 8.)